Growth can look exciting on paper and still feel stressful in the bank account.

Your Shopify revenue might be increasing. Your Meta Ads or Google Shopping campaigns might be generating sales. Your best-selling product might be moving faster than expected.

But behind the scenes, cash can still feel tight.

Inventory needs to be reordered before the last batch has fully sold. Ad platforms need budget before revenue lands. Shipping, fulfilment, refunds, payment fees, supplier deposits and product costs all need to be paid before you know how much profit is actually left.

This is why revenue-based funding can look attractive for ecommerce brands.

Instead of giving up equity or taking on a traditional fixed repayment loan, revenue-based funding gives a business capital upfront and collects repayments from future revenue. For Shopify and ecommerce brands with regular sales, it can feel like a flexible way to fund inventory, marketing, product expansion or seasonal demand.

But there is one important catch.

Revenue-based funding is repaid from revenue, not profit.

That means it can be useful when your unit economics are strong, your margins are clear and the funding is being used for a proven growth opportunity. It can also become risky when your products are already thin-margin, your ad spend is inefficient or your profitability is unclear.

This guide explains how revenue-based funding works, when it can make sense for ecommerce brands, when it becomes risky, and how to decide whether your store can afford it.

What is revenue-based funding?

Revenue-based funding, also called revenue-based financing, is a funding model where a business receives capital upfront and repays the provider using a percentage of future revenue until an agreed repayment amount is reached.

The exact structure varies by provider, but most offers include:

- A funding amount

- A repayment percentage

- A total repayment amount or repayment cap

- A repayment schedule linked to sales activity

- Eligibility criteria based on revenue, sales history or platform data

For ecommerce brands, the provider may review data from Shopify, WooCommerce, Stripe, PayPal, Amazon, marketplaces or other sales channels to assess whether the business qualifies.

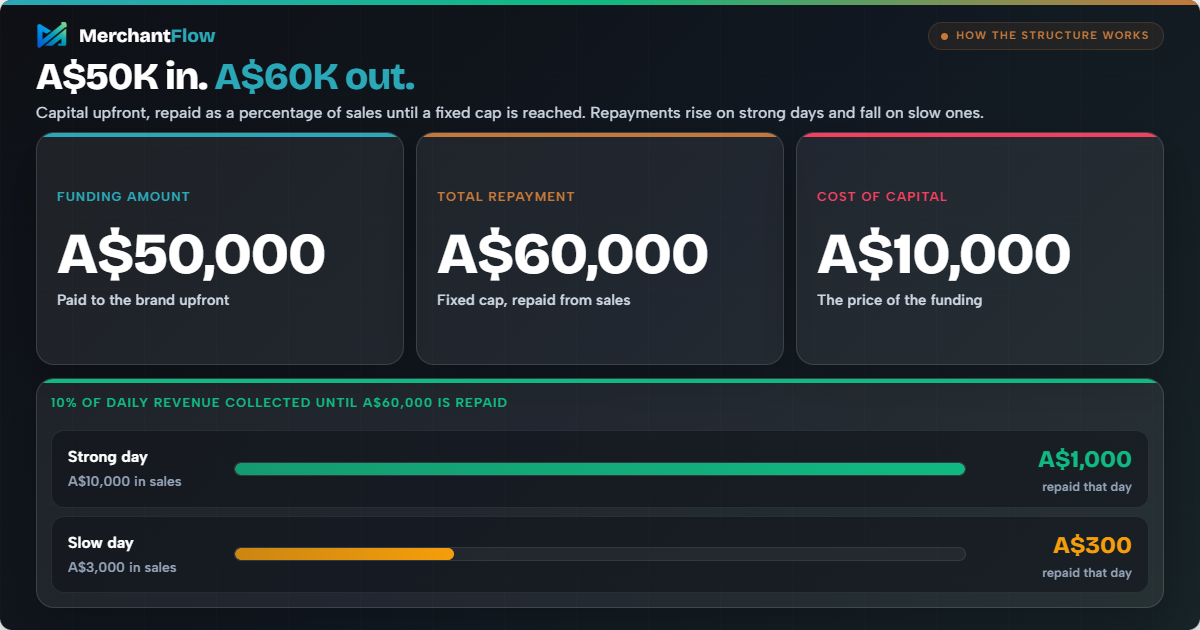

A simple example:

An ecommerce brand receives A$50,000 in funding. The agreed repayment amount is A$60,000. The provider collects 10% of daily revenue until the A$60,000 has been repaid.

On stronger sales days, the repayment amount is higher. On slower sales days, the repayment amount is lower.

That flexibility is one of the main reasons ecommerce brands consider this type of funding. It can feel more aligned with fluctuating sales than a fixed monthly repayment.

However, the repayment is usually tied to sales, not margin.

If your store generates A$10,000 in daily revenue but only A$1,200 in contribution profit after product costs, shipping, fulfilment, refunds, payment fees and ad spend, a 10% revenue repayment could consume most of the profit generated that day.

Revenue-based funding can help with cash flow, but it does not fix weak margins.

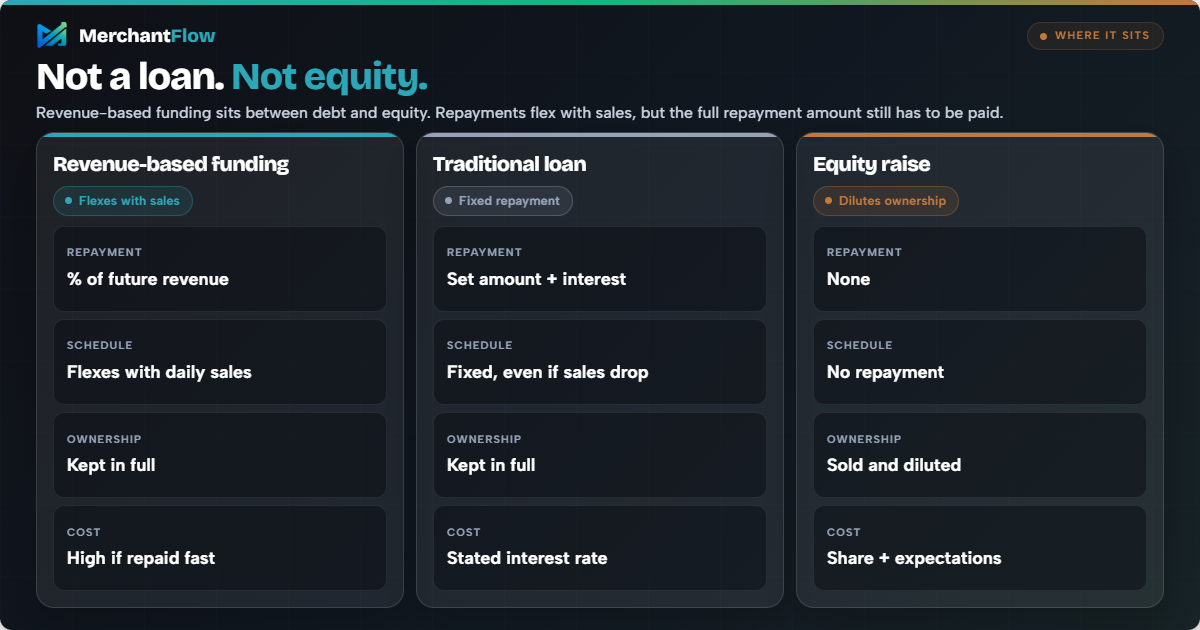

How revenue-based funding differs from a loan or equity raise

Revenue-based funding sits somewhere between traditional debt and equity finance.

With a traditional business loan, you usually borrow a set amount and repay it on a fixed schedule, often with interest. Those repayments may stay the same even if sales drop.

With equity funding, you raise capital by selling part of the business. This can reduce short-term cash pressure, but it dilutes ownership and may come with investor expectations around growth, reporting and exit outcomes.

Revenue-based funding is different because repayments are connected to sales performance. This can make it appealing for ecommerce brands with seasonal demand, fluctuating revenue or short-term working capital needs.

The trade-off is that it can be expensive relative to other funding options, especially if the repayment happens quickly. It can also reduce available cash during the exact period when the brand is trying to scale.

The real question is not:

“Can we get funded?”

The better question is:

“Can our profit model handle the repayment?”

Common revenue-based funding options for ecommerce brands

Revenue-based funding can come from a few different places.

Some ecommerce platforms offer their own funding products. Shopify Capital, for example, is available to eligible Shopify merchants in selected regions and repayments may be linked to daily store sales.

Payment platforms may also offer funding based on payment activity. Stripe Capital and PayPal Working Capital are examples of funding products that use payment or sales history to assess eligibility and collect repayments through a percentage of future sales.

There are also specialist ecommerce funding providers, such as Wayflyer, that focus on working capital for online brands. These providers often position funding around common ecommerce needs such as inventory, marketing, wholesale orders or growth capital.

The right option depends on your business model, where your revenue flows, how predictable your sales are and what the funds will be used for.

For example, a Shopify brand with most revenue flowing through Shopify Payments may look at Shopify Capital. A brand processing most payments through Stripe may consider Stripe Capital. A fast-growing ecommerce brand that needs capital for inventory or paid acquisition may compare specialist providers such as Wayflyer.

But the provider matters less than the repayment impact.

Whether the offer comes from Shopify, Stripe, PayPal, Wayflyer or another funding provider, the same question applies:

Can your products, campaigns and margins carry the repayment after COGS, shipping, refunds, fulfilment, payment fees and ad spend?

Why ecommerce brands consider revenue-based funding

Revenue-based funding is popular in ecommerce because online stores often have a timing problem.

A brand might need to pay suppliers weeks or months before stock is sold. A campaign might need ad budget before revenue arrives. A store might be preparing for Black Friday, a new product launch or international expansion and need cash before the sales cycle catches up.

Common reasons ecommerce brands consider revenue-based funding include:

- Buying inventory for a proven product

- Scaling profitable Meta Ads, Google Shopping or Performance Max campaigns

- Funding a seasonal stock build

- Launching a new product line

- Covering supplier deposits

- Managing cash flow between order volume and fulfilment costs

- Avoiding equity dilution

Used carefully, funding can help a brand capture demand it would otherwise miss.

For example, a skincare brand might have a hero product that regularly sells out. The product has healthy margin, strong repeat purchase behaviour, low refund rates and consistent paid acquisition performance. In that case, funding a larger inventory order could make sense if the expected profit comfortably exceeds the cost of the capital.

But the same funding can be dangerous if it is used to scale an unproven product, cover operating losses or push more budget into ads that only look profitable inside the ad platform.

How to decide which funding option makes sense

Do not choose a funding option only because it is easy to access or already built into a platform you use.

Start with the use case.

If the funding is for inventory, check whether the product has proven sell-through, healthy contribution margin and reliable demand. If the funding is for ad spend, check whether the campaigns are profitable after COGS, shipping, refunds, payment fees and fulfilment costs. If the funding is for cash flow, check whether the gap is temporary or whether the business is relying on new funding to cover ongoing losses.

Then look at the repayment terms.

Compare the total repayment amount, repayment percentage, collection frequency, minimum repayment requirements, fees, refund treatment and what happens if sales slow down.

The best funding option is not always the one with the fastest approval or the largest offer. It is the one your margin structure can handle without putting pressure on inventory, tax, wages, ad spend or supplier payments.

The biggest mistake: funding revenue instead of profit

The most common mistake is using revenue-based funding to chase top-line growth without understanding contribution margin.

Revenue can make the business look healthy. Profit shows whether the growth is actually working.

A store might generate A$100,000 in monthly revenue and still have very little cash left after:

- Cost of goods sold

- Shipping and fulfilment

- Discounts

- Refunds and returns

- Payment processing fees

- Platform fees

- Ad spend

- Agency fees

- Packaging

- Duties or import costs

- Revenue-based funding repayments

This matters because many funding offers are assessed against revenue. But your ability to repay safely depends on profit and cash flow.

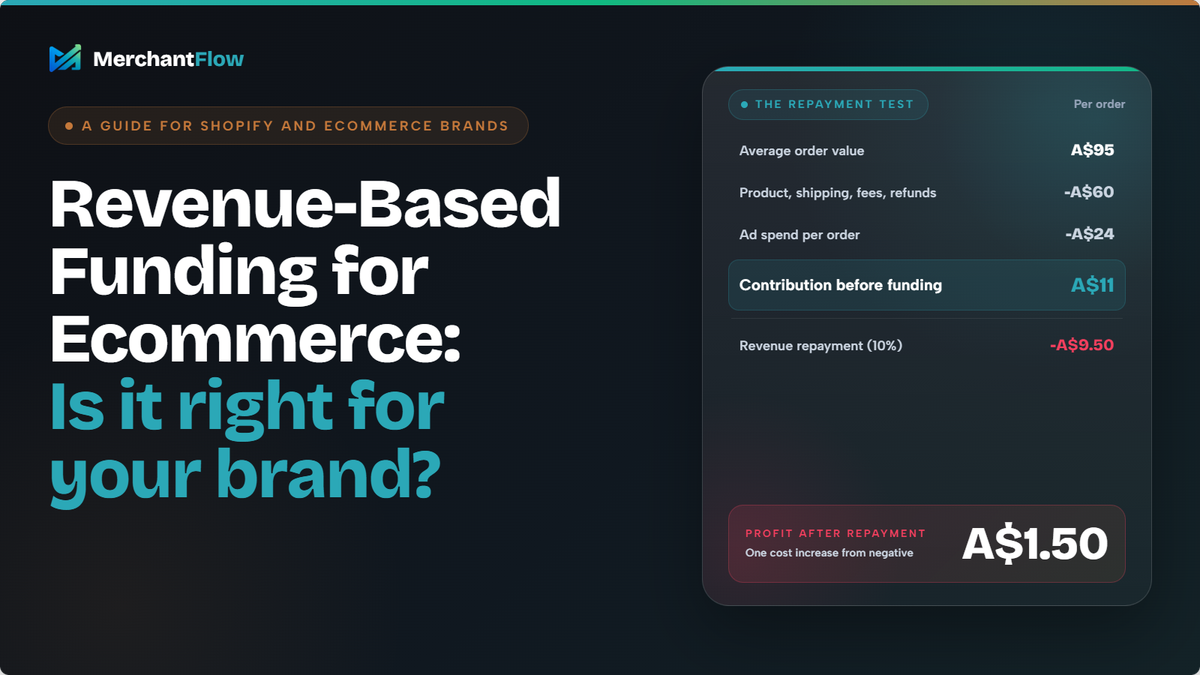

Here is a simple product-level example.

| Metric | Amount per order |

|---|---|

| Average order value | A$95 |

| Product cost | A$38 |

| Shipping and fulfilment | A$12 |

| Payment fees | A$3 |

| Refunds and discounts allowance | A$7 |

| Gross contribution before ads | A$35 |

| Ad spend per order | A$24 |

| Contribution profit before funding repayment | A$11 |

| Revenue-based repayment at 10% of revenue | A$9.50 |

| Contribution profit after repayment | A$1.50 |

At first glance, this product looks profitable. It generates A$11 per order after ad spend.

But once a 10% revenue-based repayment is included, the product only contributes A$1.50 per order. A small increase in ad costs, refund rates, shipping costs or discounting could push it into negative margin.

This is why revenue-based funding should not be assessed using revenue alone. You need to know whether your main products, campaigns, channels and regions can still produce profit after the repayment is included.

When revenue-based funding can make sense

Revenue-based funding can be a good option when it supports a proven growth opportunity.

It is usually strongest when the brand already has clear demand, healthy margins and a specific use for the funds.

You have a proven product with healthy margins

Funding is easier to justify when you are putting capital behind a product that already works.

For example, if your best-selling product has strong repeat purchases, stable supplier costs, low refund rates and healthy contribution margin after ad spend, funding a larger inventory order may help you avoid stockouts and capture more demand.

The key is knowing the product is profitable at the unit level.

If you only know store-wide revenue, you are guessing.

You have predictable paid acquisition performance

Some brands use revenue-based funding to scale ads. This can work, but only if the acquisition economics are already proven.

Before using funding for Google Shopping, Meta Ads, TikTok Ads or Performance Max, you should understand:

- Blended CAC

- Product-level ROAS

- Contribution margin after ad spend

- Refund and return rates by product

- Payback period

- How performance changes when budget increases

A campaign that works at A$300 per day may not work at A$1,000 per day. Scaling budget can change CPMs, conversion rates, audience quality and cash flow.

Funding can amplify a good system. It can also amplify an inefficient one.

You are solving a short-term cash flow gap

Revenue-based funding may suit a brand with a temporary cash flow gap.

For example, a fashion brand preparing for summer might know that demand increases from October to December. If historical data shows those products sell through profitably, funding inventory before the season could be reasonable.

The danger is using short-term funding for ongoing operating losses.

If the brand needs new funding every few months just to keep moving, the issue may not be access to capital. It may be pricing, margin, ad efficiency, stock management or cost control.

You want to avoid equity dilution

For founder-led ecommerce brands, avoiding dilution can be appealing.

Revenue-based funding does not usually require selling ownership in the company. That can make it useful for brands that want capital without bringing on investors.

However, non-dilutive does not automatically mean cheap.

A funding option can avoid equity dilution and still be expensive if the repayment burden weakens cash flow or erodes contribution margin.

When revenue-based funding becomes risky

Revenue-based funding is not automatically bad. It becomes risky when the brand does not have enough visibility over profitability.

Your margins are already thin

If your contribution margin is low, revenue-based repayments can quickly absorb the profit that remains.

This is common in categories with:

- Heavy discounting

- High return rates

- Expensive shipping

- Bulky products

- Low repeat purchase rates

- High paid acquisition costs

- Import duties or volatile supplier costs

A product with strong contribution margin may have enough room to absorb a repayment. A product with thin margin may not, especially after ads, fulfilment and refunds.

You are relying on platform ROAS

Platform ROAS can be useful, but it is not the same as profit.

Google Ads, Meta Ads and TikTok Ads can show revenue attributed to campaigns. They do not automatically show whether that revenue was profitable after product costs, shipping, refunds, payment fees and fulfilment.

A campaign with 3.0 ROAS might be profitable for a high-margin product and unprofitable for a low-margin product.

If you use revenue-based funding to scale ads based only on ROAS, you may be borrowing money to grow a loss-making channel.

You do not know your product-level profitability

Store-wide averages can hide serious problems.

One product might generate most of your revenue but very little profit after shipping and ad spend. Another product might have lower revenue but much stronger contribution margin. A third product might look strong until refunds are included.

Revenue-based funding is repaid from total sales, but the cash flow impact is felt across the whole business.

If you do not know which products are actually funding the business, you risk using capital to scale the wrong parts of the store.

Your sales are volatile

Revenue-based repayments may flex with sales, but the total repayment amount still needs to be paid.

If sales drop because of seasonality, stock delays, ad account issues, feed disapprovals or weaker demand, repayments may slow down, but your other costs continue.

This can create pressure if the funding has already been committed to inventory, ads or supplier payments.

You are using funding to avoid hard decisions

Sometimes funding feels like a solution because it delays difficult operational decisions.

For example:

- Prices may need to increase

- Unprofitable products may need to be cut

- Free shipping thresholds may need to change

- Discounts may need to be reduced

- Ad campaigns may need to be restructured

- COGS may need to be renegotiated

- Returns may need deeper analysis

If the underlying issue is profitability, more cash may only buy time.

The ecommerce funding test: can your unit economics carry the repayment?

Before accepting revenue-based funding, run a simple profitability stress test.

Start with your major products and calculate contribution margin before and after the proposed repayment rate.

At a minimum, you should know:

- Revenue by product

- Cost of goods sold

- Shipping and fulfilment cost

- Payment fees

- Refunds and discounts

- Ad spend by channel

- Contribution margin before repayment

- Proposed repayment as a percentage of revenue

- Contribution margin after repayment

Then ask:

Would this still be profitable if ad costs increased by 15% or conversion rate dropped by 10%?

If the answer is no, the funding may be too tight for the current model.

A brand should not assess funding based only on its best month. It should model a realistic month, a slow month and a growth month.

That gives a clearer view of whether the repayment is manageable or whether it could turn normal performance fluctuations into cash pressure.

If you are comparing offers, MerchantFlow’s free Revenue-Based Financing Calculator can help you model the funding amount, total repayment amount, repayment percentage and potential cash flow impact before you commit.

It will not tell you whether a funding offer is automatically good or bad, but it can help you understand the repayment pressure. From there, you can compare the offer against your product-level margins, ad spend, COGS, shipping, refunds and fulfilment costs.

How revenue-based funding affects ad spend decisions

Funding and advertising are closely linked in ecommerce.

Many brands consider revenue-based funding because they want to increase ad spend. That can be reasonable if the campaigns are profitable and the brand has enough inventory to fulfil the extra demand.

But ad spend is not just a growth lever. It is also a cash flow commitment.

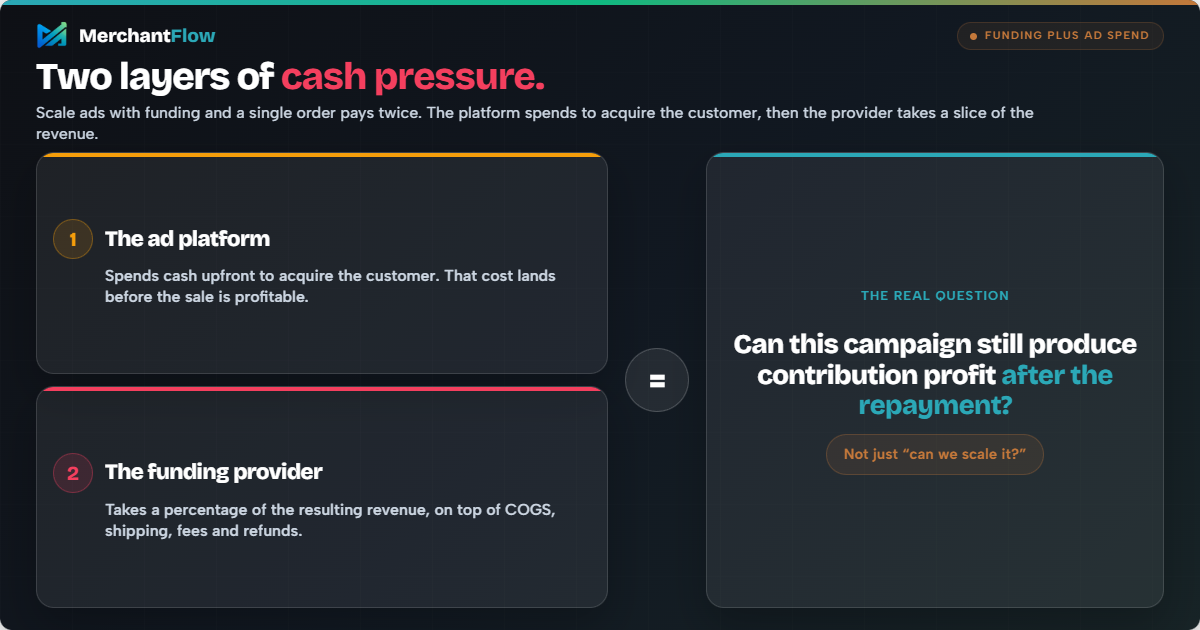

If you use funding to scale Meta Ads or Google Shopping, you are adding two layers of pressure:

First, the ad platform spends cash to acquire the customer.

Second, the funding provider takes a percentage of the resulting revenue.

That means your campaign needs to cover product costs, fulfilment, payment fees, refunds, discounts, ad spend and the funding repayment.

A better question than:

“Can we scale this campaign?”

is:

“Can this campaign still produce contribution profit after the funding repayment?”

For Google Shopping and Performance Max, feed quality also matters. If product data is inaccurate, key products are disapproved, pricing is mismatched or availability is wrong, your paid growth plan may be constrained before funding even enters the picture.

The stronger your visibility across product profitability, feed health and ad spend, the safer your funding decision becomes.

Three practical ecommerce examples

Example 1: Funding makes sense

A Shopify brand sells a hero supplement product with strong repeat purchase behaviour.

The brand knows:

- Gross margin is healthy

- Contribution margin after ads is strong

- Refund rates are low

- Subscription purchase rate is growing

- Google Shopping campaigns are stable

- The main constraint is inventory availability

The brand receives a revenue-based funding offer and uses it to place a larger inventory order before a proven seasonal demand period.

In this case, funding may make sense because the use of funds is clear, the product economics are strong and the capital helps solve a real growth constraint.

Example 2: Funding looks attractive but creates risk

A fashion brand has strong revenue, but high return rates, frequent discounting and rising Meta Ads costs.

The founder receives a funding offer and plans to use it to increase ad spend.

The issue is that product-level profitability is unclear. Some products are profitable, but others lose money after returns and shipping. The brand is looking at blended ROAS, not contribution margin.

In this case, revenue-based funding could make the problem worse. The brand may scale revenue while reducing cash flow and profit.

Before taking funding, the brand should identify which products can absorb the repayment and which campaigns need to be reduced or restructured.

Example 3: Regional revenue hides margin problems

A brand expands from Australia into the United States.

US revenue grows quickly, but shipping costs, duties, fulfilment complexity and customer support costs are higher than expected. The US market looks exciting in Shopify and ad platforms, but profit by region tells a different story.

If the brand takes funding to scale US growth based only on revenue, it may end up funding a lower-margin market.

This is where margin by region becomes important. A country with higher revenue is not always the country with stronger profit.

Questions to ask before accepting revenue-based funding

Before signing anything, review the offer like a cash flow decision, not a growth milestone.

Repayment terms

Ask:

- What is the total repayment amount?

- What percentage of revenue will be collected?

- Are repayments taken daily, weekly or monthly?

- Are repayments based on gross sales, net sales or processed payments?

- Are there minimum repayment requirements?

- Is there a maximum repayment period?

Fees and conditions

Ask:

- Are there origination fees, platform fees or early repayment fees?

- Can the repayment percentage change?

- What happens if sales drop?

- How are refunds treated?

- Are personal guarantees required?

- Can you take additional funding before the first amount is repaid?

Business impact

Ask:

- How will the repayment affect cash available for inventory, ads, wages and tax?

- Which products will generate the profit needed to repay it?

- Which campaigns will carry the repayment burden?

- What happens if ad costs rise or conversion rates fall?

- Will the funding improve the business, or just delay a cash flow problem?

If you cannot answer these questions clearly, the offer may be premature.

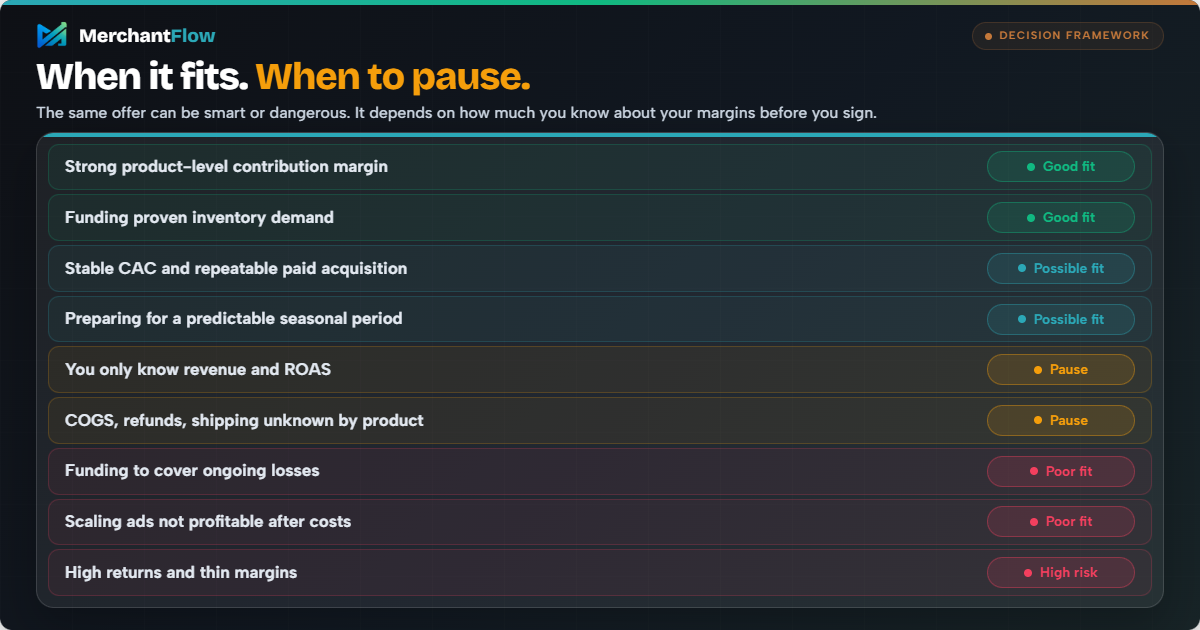

A simple decision framework

Revenue-based funding may be worth considering if the funding supports a proven, profitable opportunity.

| Situation | Funding fit |

| You have strong product-level contribution margin | Good fit |

| You are funding proven inventory demand | Good fit |

| You have stable CAC and repeatable paid acquisition | Possible fit |

| You are preparing for a predictable seasonal sales period | Possible fit |

| You only know revenue and ROAS | Pause |

| You do not know COGS, refunds or shipping by product | Pause |

| You are using funding to cover ongoing losses | Poor fit |

| You are scaling ads that are not profitable after costs | Poor fit |

| You have high returns and thin margins | High risk |

“Pause” does not always mean “do not take funding”.

It means you should improve visibility before making the decision.

The safest use case is funding a proven, profitable growth constraint. The riskiest use case is using funding because the business does not yet understand why cash is tight.

Alternatives to revenue-based funding

Revenue-based funding is only one option. Depending on your brand’s stage, risk profile and cash flow, other options may be more suitable.

You could consider:

- Negotiating better supplier payment terms

- Improving inventory forecasting

- Reducing slow-moving stock

- Increasing prices on low-margin products

- Adjusting free shipping thresholds

- Reducing discounts

- Using a traditional business loan or line of credit

- Using platform-based funding where available

- Raising equity if the business needs long-term growth capital

- Slowing growth temporarily to improve profitability first

Sometimes the best funding decision is not to take funding yet.

If a brand improves margin, cleans up product data, reduces wasted ad spend and fixes pricing, it may need less capital than expected.

How MerchantFlow helps brands make better funding decisions

Revenue-based funding is ultimately a profitability decision.

Before taking capital, ecommerce brands need to understand which products, campaigns, channels and regions are actually making money after costs.

That is difficult when revenue lives in Shopify, ad spend lives across Google, Meta, TikTok or other platforms, product costs live in spreadsheets, and shipping, refunds, payment fees and fulfilment costs are analysed separately.

MerchantFlow helps Shopify and ecommerce businesses bring those numbers into one profit-focused view.

That means you can answer questions like:

- Which products have enough margin to absorb a funding repayment?

- Which campaigns are profitable after ad spend and COGS?

- Which regions generate revenue but weak contribution margin?

- How much profit is left after refunds, shipping and fees?

- Are we scaling products that make money, or just products that sell?

- What happens to contribution margin if we add a 5%, 8% or 10% revenue repayment?

Revenue-based funding can be useful, but only when you have the numbers to use it confidently.

The goal is not just to grow faster. It is to grow profitably.

Revenue Based Funding FAQs

Is revenue-based funding a good idea for ecommerce brands?

Revenue-based funding can be a good option for ecommerce brands with proven demand, healthy margins and a clear use of funds. It is usually better suited to funding inventory, seasonal demand or profitable campaign expansion than covering ongoing losses.

The key is knowing whether your contribution margin can absorb the repayments.

Is revenue-based funding the same as Shopify Capital?

Not exactly. Shopify Capital is a platform-based funding option available to eligible Shopify merchants. Revenue-based funding is a broader category that may be offered by different providers using ecommerce, payment processor or marketplace revenue data.

The important point is to understand the repayment structure, total repayment amount, fees and cash flow impact before accepting any funding offer.

Can I use revenue-based funding to buy inventory?

Yes, inventory is often one of the better use cases for revenue-based funding, but only when the products are already proven.

If you know the product sells through profitably, has healthy contribution margin and has reliable demand, funding inventory can help prevent stockouts. If the product is unproven or slow-moving, funding can create more risk.

Can I use revenue-based funding to scale Meta Ads or Google Shopping?

You can, but you should be careful.

Funding ad spend only makes sense if your campaigns are profitable after product costs, shipping, refunds, payment fees and the funding repayment. Do not rely only on platform ROAS. Look at contribution margin after ad spend.

Is revenue-based funding expensive?

It can be. The cost depends on the funding amount, total repayment amount, fees, repayment percentage and how quickly the funding is repaid.

A funding offer can look simple because there may be no traditional interest rate, but the effective cost can still be high. Always calculate the total repayment and model how it affects product-level and store-level profit.

What repayment percentage is safe?

There is no universal safe percentage.

A 5% repayment may be manageable for a high-margin brand and risky for a low-margin brand. The right way to assess it is to model contribution margin after the repayment across your main products, channels and regions.

What should I check before accepting revenue-based funding?

Check the total repayment amount, repayment percentage, repayment schedule, fees, minimum repayment rules, refund treatment and impact on cash flow.

You should also check product-level profitability, campaign profitability and whether the funding is being used for a proven growth opportunity.

What is the biggest risk of revenue-based funding?

The biggest risk is using funding to grow revenue without understanding profit.

Because repayments are often tied to revenue, not profit, a brand can increase sales while reducing cash flow if margins are weak, ad spend is inefficient or refund and shipping costs are higher than expected.

Final thoughts

Revenue-based funding is not good or bad on its own. It depends on the strength of your ecommerce economics.

If you have proven demand, clear product-level margins and a specific use for the capital, funding can help you capture growth that would otherwise be delayed.

If your numbers are unclear, funding can make the business feel bigger while quietly making it less profitable.

Before accepting an offer, make sure you know what your products, campaigns, channels and regions are actually contributing after costs.

MerchantFlow helps ecommerce brands see true profitability across revenue, ad spend, COGS, shipping, refunds, payment fees and fulfilment costs, so funding decisions can be made with clarity rather than guesswork.

If you are considering revenue-based funding, start by understanding whether your store can still grow profitably after the repayment.

About the author

Georgia CarapetisGeorgia Carapetis is Head of Marketing at MerchantFlow, helping ecommerce brands stop obsessing over ROAS and start focusing on profit. She writes about Google Shopping, contribution margins, and scaling without shrinking your margins.